EMV is an acronym that stands for Europay, MasterCard and Visa. They are the founding companies for chip card technology. EMV is a payment application that resides in a computer chip embedded in a debit card. The application specifications were developed to help fight fraud. The term ‘EMV’ and ‘chip card’ are interchangeable.

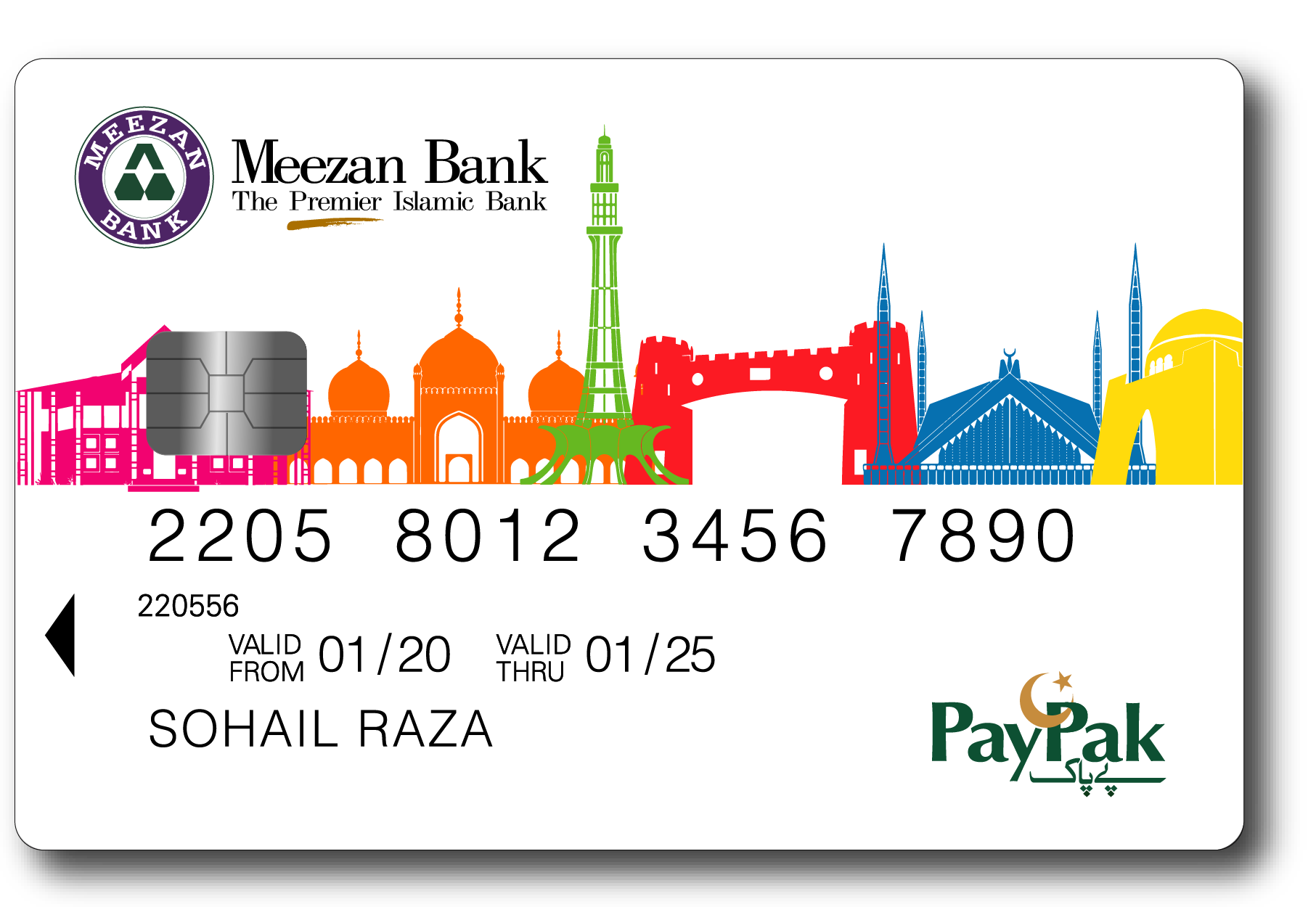

All new Meezan Bank Debit Cards are EMV and NFC enabled. To get your new EMV NFC card, simply contact our Call Center at (+9221) 111-331-331 or 111-331-332 or visit your branch to get your new card. Replacement charges will be applicable.

NFC cards use an embedded radio frequency antenna and microchip that allows a transaction to be processed by simply tapping the card on a merchant’s payment terminal instead of swipe and signature on receipt.

NFC card transactions are processed through the same secured networks used for Visa and MasterCard transactions. You never lose sight of your card while each transaction has a unique, encrypted code that changes every time the card is used.

Below are some of the security features available on NFC Debit Card:

- Short Range:

The card only works within short range of a merchant terminal, which makes it difficult for fraudsters to gain access to card information from a distance.

- Encryption:

NFC cards use much more secure international EMV chip standards and advanced cryptography. During a transaction, a unique encryption code is shared between the card and device which expires after every transaction. If someone were able to get close enough to steal data from your card, they would still be unable to use the encryption code as it would have been expired.

- Limited Information: Only limited information is used in a ‘Tap and Pay’ transaction like language preference, card number and other coding. Customer’s name, bank account number or the three-digit security code is not transmitted during a transaction.

- Transaction Limit: To improve customer convenience and streamline the checkout process, contactless payments up to PKR 3,000 per transaction (limit may vary by bank) can be made without entering a PIN. Transactions exceeding this limit will require a PIN.

During a payment transaction, the chip performs cryptographic processing by assigning a unique code to each transaction. This helps prevent the transaction data from being fraudulently reused. Chip processing takes place only when the card is used at a chip-activated terminal.

A chip terminal is a point-of-sale (POS) device or ATM that is able to process chip transactions. Instead of swiping your card, you insert it in a chip terminal and leave it in the terminal until the transaction is complete. If a merchant does not have a chip terminal or if their chip terminal is not yet activated, transactions will be processed by swiping the card’s magnetic stripe just as they are processed today.

Make sure you remove your card from the terminal before leaving the merchant’s premises! This is a common challenge people face when getting used to using a chip card.

Both chip and magnetic stripe card transactions are processed very quickly. Leaving your card inserted, versus swiping the card, does add a few seconds on to the transaction in order to assign the unique code to your transaction. This is a step that does not exist with magnetic stripe only transactions; and, it is what adds the additional layer of security.

No. There are several manufacturers and styles of chip terminals. However, all terminals perform the same function of inserting the chip and assigning a unique code to each transaction.

You will be required to sign for all your debit card purchases. However some merchants may require you to enter your PIN to complete a transaction if the merchant’s terminal supports PIN entry.

Both ‘chip and signature' and ‘chip and PIN’ refer to the way a card is authenticated at the terminal. Your card will be authenticated using chip and signature, which offers the same cryptographic security as chip and PIN.

Most merchant terminals will require the chip to be used if the terminal is enabled to accept chip transactions. The terminal should prompt you to use your chip when it is a requirement. Using the chip is a more secure transaction method than magnetic stripe-only at point-of-sale, so this is the preferred method where merchants have enabled chip transactions.

Yes. At ATMs that are not chip-enabled, the transaction will be processed using your card’s magnetic stripe technology in combination with your PIN. At ATMs equipped with chip readers, the transaction will be processed using the chip technology in combination with your PIN.

We take card security very seriously and have sophisticated fraud detection services in place:

- 24/7 Fraud Monitoring – We always monitor your accounts for suspicious activity and attempt to contact you when we see something out of the ordinary.

- SMS Alert Service – You will receive alerts for your purchase transactions by default on your registered mobile number. You may also opt for SMS alert service (additional fee applicable) to receive transaction alerts on all account activities.

on the POS machine.

on the POS machine.